Africa's B2B Payments Gap: World-Class Rails, WhatsApp Invoicing

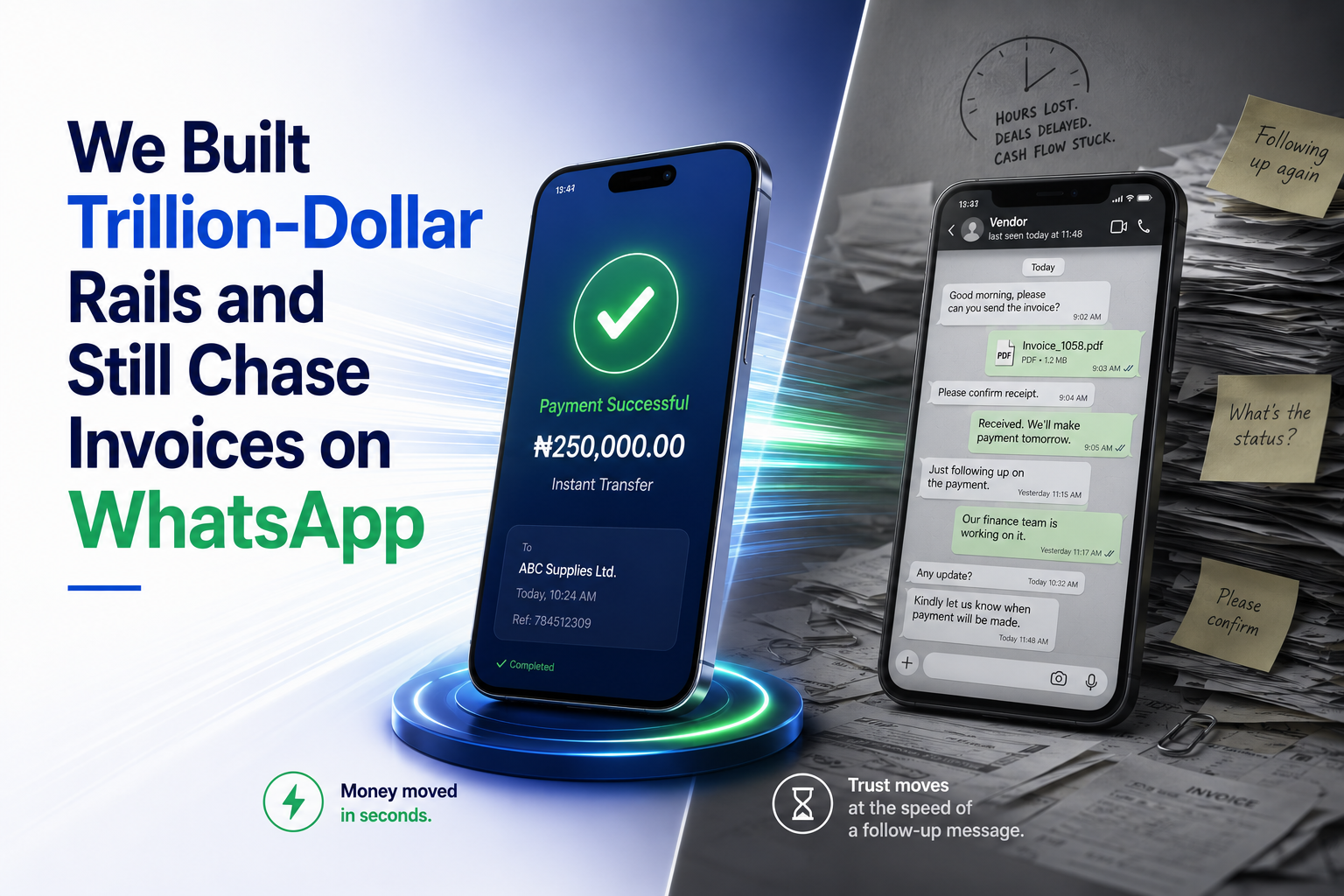

We Built Trillion-Dollar Rails and Still Chase Invoices on WhatsApp

Last year, more than 1.4 trillion dollars moved through mobile money in Sub-Saharan Africa. Sit with that number. It is roughly two thirds of all the mobile money value moved on earth, generated on one continent, by people sending and receiving money on their phones in seconds. Globally, mobile money took twenty years to reach its first trillion dollars in annual value, and just four more to double to two. Africa did not catch up to the rest of the world on consumer payments. It ran ahead.

And yet, this morning, somewhere in Lagos or Nairobi or Accra, a finance officer is opening WhatsApp to chase an invoice.

Two Realities, One Continent

Here is the contradiction nobody quite says out loud. The same person who splits a restaurant bill in three taps on a Saturday spends Monday morning hunting a business payment through bank apps, email threads, and a spreadsheet.

The rails work. Nigeria's instant payment system moved over a quadrillion naira in a single year. M-Pesa alone handled tens of trillions of shillings across billions of transactions. Forty percent of adults in Sub-Saharan Africa now hold a mobile money account, the highest rate of any region on the planet. When it comes to moving consumer money, the trust is instant, and both sides simply believe it landed.

Then a business has to pay another business, and that same trust collapses back into the stone age. According to one survey of African business owners, 44 percent wait more than a day just to be paid, and many wait a week or a month. Not because the money cannot move. The money moves in seconds. It is everything around the money that is still stuck.

Why the Gap Exists

The reason is simple once you see it. Consumer mobile money solved one clean problem: move value from one phone to another, instantly, with trust anchored to a number and a PIN. That is the whole job, and Africa nailed it.

Business payments are a harder thing entirely. A B2B payment is not just a transfer. It is an invoice with terms, an approval, a matching process, a reconciliation, and trust between more than two parties. The rails were built to move money. They were never built to carry the invoice, which is where the actual promise lives.

So when a buyer makes a bank transfer, the receiving business sees an amount and a sender name, and nothing else. No invoice reference. No context. Someone has to become a detective, matching payments to invoices by hand. The rail did its job in seconds. The invoice turned it back into days of work.

What the Gap Costs

This is not a small inconvenience. It is a tax on growth.

Money owed but not yet collected is working capital you cannot deploy. Across borders it gets worse: before pan-African settlement systems existed, more than 80 percent of African cross-border payments had to be routed offshore to clear, and the friction is estimated to cost the continent around 5 billion dollars a year. All of that sits on top of an intra-African trade opportunity the World Bank values in the hundreds of billions. The rails are ready for that future. The invoicing is not.

The Opportunity

Here is the optimistic part, and it is the whole point. Africa has already proven it can leap. It did it once, for consumers, and led the world. The same leap simply has not happened yet for business.

That is not a weakness. It is the clearest opportunity on the continent. The infrastructure to make business trust move as fast as consumer trust already does, structured invoicing, automatic approval, instant settlement, and reconciliation that happens by itself, is the next frontier. And it is already starting. Nigeria is now mandating structured, government-validated e-invoicing, which tells you the direction of travel. The question is who builds for it early.

The Takeaway

We built trillion-dollar rails and then accepted that the invoice, the most important document in any business relationship, would keep crawling along behind them on WhatsApp. That gap between fast money and slow trust is the real story of African B2B payments.

The businesses that close it first, that make getting paid as instant and certain as sending money to a friend, will not just save time. They will move at a speed their competitors cannot match.

Ready to make your business payments move as fast as your phone already does? See how Curacel Pay closes the loop from invoice to settlement at curacel.co.

See how Pay AI works --> curacel.co/curacel-pay

Abonnez-vous à notre newsletter pour recevoir du contenu hebdomadaire

.svg)