Embedded Insurance for Fintechs and Banks: How to Ship Coverage That Actually Works at Scale

Every fintech and digital bank in Africa already has customers who face financial risk. The question is whether those platforms are capturing the value of protecting against that risk, or leaving it for someone else to monetise.

Embedded insurance integrates coverage directly into a non-insurance platform at the point where risk is most relevant: a logistics company offering goods-in-transit cover at checkout, a digital lender bundling credit life into a loan disbursement, a ride-hailing app activating accident cover the moment a driver goes online. The coverage isn’t sold separately. It’s built into the transaction, activated automatically or with a single opt-in, and managed through API infrastructure the end customer never sees.

According to the Open and Embedded Insurance Observatory’s 2024 report, embedded insurance is on track to account for 15% of global gross written premiums by 2033, representing approximately $1.1 trillion. Mordor Intelligence estimates the global market will grow from $210.9 billion in 2025 to $950.6 billion by 2030. In Africa specifically, ResearchAndMarkets projects the continent’s embedded finance market will reach $18 billion by 2030, with insurance as one of the fastest-growing verticals.

Here’s the practical playbook for shipping it cleanly.

What Embedded Insurance Actually Is (and the 3 Models That Work)

Embedded insurance isn’t one thing. There are three models worth understanding:

Add-on — Insurance offered as an optional extra at the point of transaction. The platform distributes, the insurer underwrites and services. Think travel cover at flight checkout or device protection at an electronics purchase.

Bundled — Insurance included as part of the core product or subscription. The customer doesn’t opt in — it’s baked into the pricing. Common in logistics (goods-in-transit) and lending (credit life at disbursement).

Mandatory / Opt-out — Regulatory or contractual requirements make insurance a default. Motor third-party coverage through ride-hailing platforms is the classic example across African markets.

Each model shifts who owns distribution, servicing, and reporting differently. And each breaks in different places when the infrastructure behind the API isn’t structured for it.

Why Africa Is Structurally Ready for This

The conditions that make embedded insurance work aren’t evenly distributed globally. Africa has several of them in concentrated form.

Massive uninsured populations. Insurance penetration across the continent averages below 3% of GDP. In Nigeria, only about 2 million people out of a population exceeding 237 million hold any form of insurance, according to the EFInA 2021 Access to Financial Services Survey. Traditional distribution has failed to reach these customers. The platforms they already use daily — for payments, lending, transport, and commerce — have not.

Mobile-first infrastructure already in place. Kenya has over 30 million active M-Pesa users. Nigeria has more than 115 million active internet users. The distribution rails exist. What’s missing is the insurance product layer sitting on top of them.

Regulatory frameworks catching up. Nigeria launched its open banking regulation in March 2024, enabling consent-based data sharing that directly supports embedded finance use cases. Kenya’s Central Bank has formalised Digital Credit Provider licensing. Egypt’s Unified Insurance Law No. 155 mandates digital insurance under Article 199. The regulatory direction is clear, even where the pace varies.

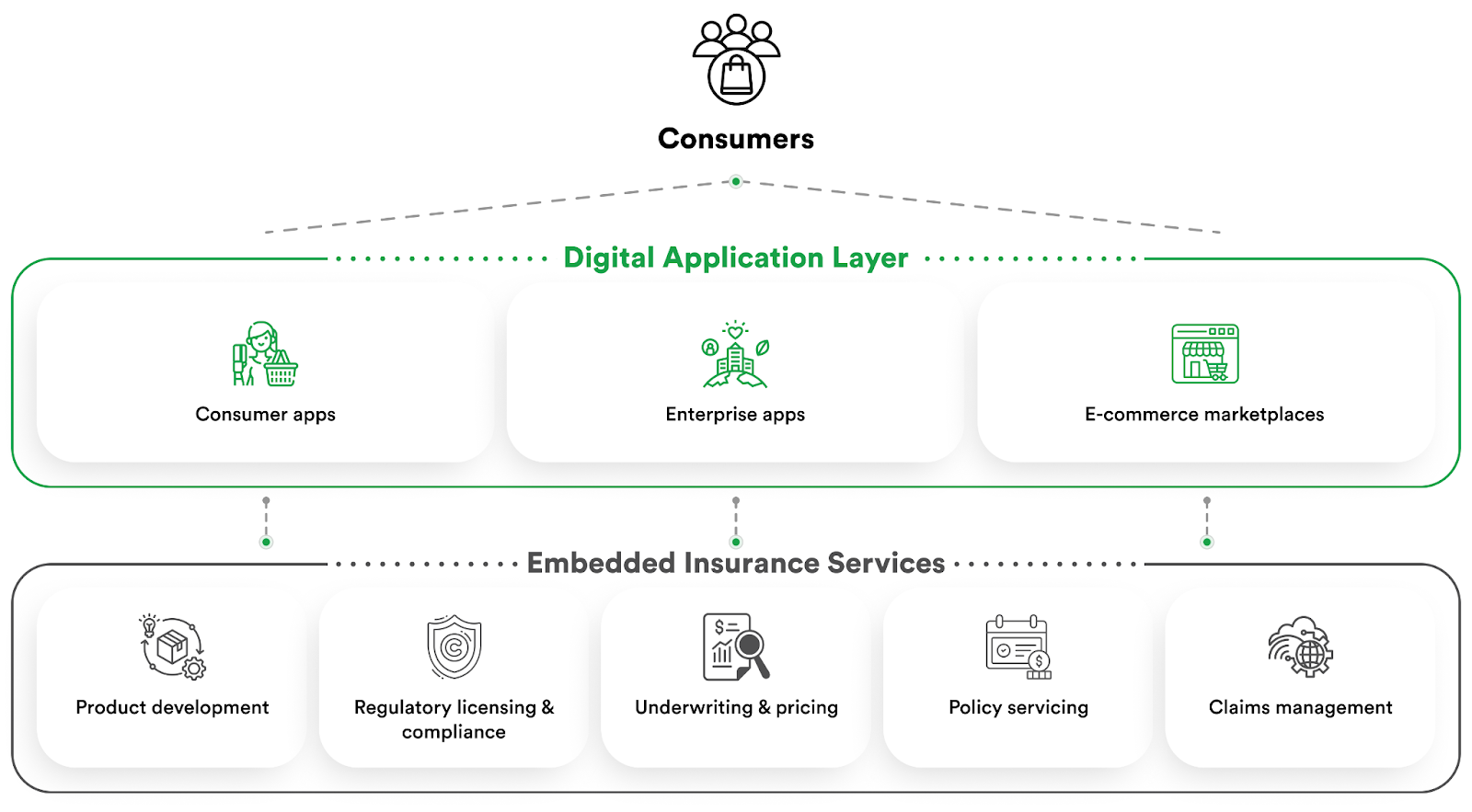

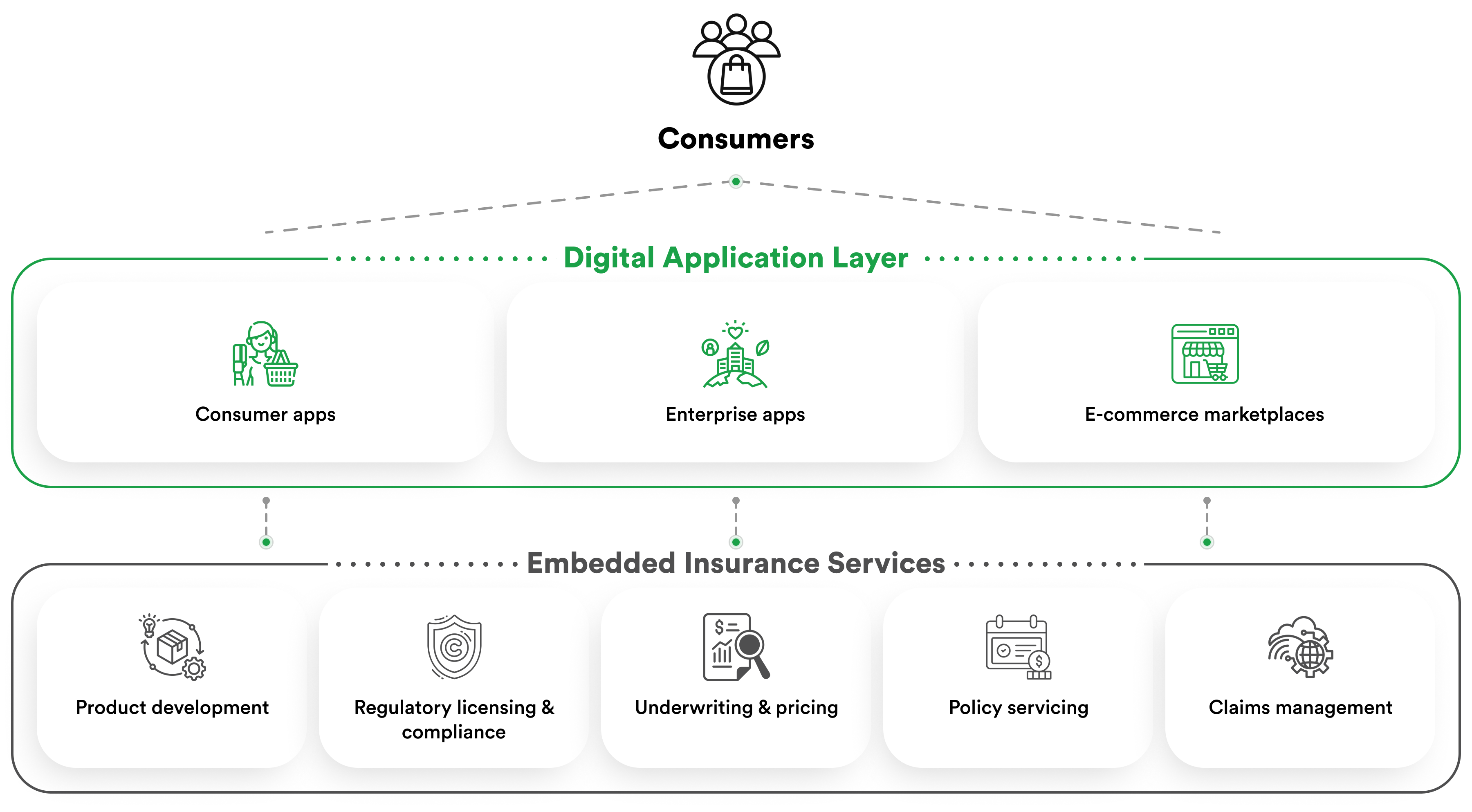

The Architecture: 5 Layers That Need to Exist

Embedded insurance sounds simple on a pitch deck. In production, it requires five layers working together. Weakness in any one produces a poor customer experience or a compliance failure.

Product engine — Configures coverage types, pricing, terms, and eligibility rules per market. Without it, every new product or market requires months of custom development.

Distribution API — Connects the platform’s user journey to the insurance product at the right moment. Bad timing or friction kills conversion. Insurance offered at the wrong step gets ignored.

Underwriter network — Routes risk to licensed carriers across multiple markets. Platforms can’t underwrite risk themselves. They need licensed partners, often different ones per country.

Fulfilment engine — Handles enrolment, policy issuance, premium collection, and certificate generation. If a customer pays but never receives confirmation, trust collapses immediately.

Servicing layer — Manages notifications, renewals, and any post-purchase support. Insurance that’s easy to buy but impossible to use destroys the platform’s reputation, not the insurer’s.

The critical insight for platform operators: when embedded insurance fails, the customer blames the platform, not the underwriter. The platform’s brand carries the experience, which means the infrastructure behind it needs to be as reliable as the platform’s own core product.

👉 Book a demo to see how Curacel’s partner distribution infrastructure handles the full stack.

Commercial Models That Work

Embedded insurance generates revenue for platforms in three primary structures, each with different margin profiles and operational requirements.

Commission on premium — The platform earns a percentage of each premium collected. This is the simplest model, requires no risk-bearing, and works well for high-frequency, low-premium products like device protection or transit cover. Typical commissions range from 15 to 30% of premium depending on product type and volume.

Revenue share on underwriting margin — The platform shares in the underwriting profit (or loss) alongside the carrier. This requires more sophisticated data sharing and risk alignment, but produces higher returns when loss ratios are favourable. It works best when the platform has proprietary data that improves risk selection.

Subscription / SaaS fee — The platform bundles insurance into its own subscription pricing and pays the underwriter a flat or per-user fee. Common in B2B platforms where coverage is part of the value proposition rather than an add-on.

The right model depends on volume, product type, and how much risk data the platform controls. Most successful implementations start with commission and evolve toward revenue share as the data matures.

Implementation Sequencing

Platforms that launch embedded insurance successfully follow a consistent pattern. They start narrow, prove the model, and expand.

Phase 1: Single product, single market (Weeks 1-6). Choose one insurance product that maps directly to an existing transaction in your platform. Integrate the API, connect to one underwriter, and launch in one market. Measure activation rate (percentage of eligible users who opt in or are auto-enrolled), premium per transaction, and customer support volume related to insurance. The goal is to validate product-market fit before adding complexity.

Phase 2: Optimise and expand coverage (Months 2-4). Refine offer placement, pricing, and messaging based on Phase 1 data. A/B test opt-in vs. bundled models. Introduce a second product line if the first is performing. Add servicing capability if customer enquiries reveal gaps.

Phase 3: Multi-market and multi-carrier (Months 4-8). Expand to additional markets, each requiring a licensed underwriter in that jurisdiction. This is where the infrastructure layer earns its value — managing carrier relationships, regulatory compliance, and product configuration across three or more markets manually is operationally unsustainable.

What to Get Right From Day One

Three decisions made at the start determine whether an embedded insurance implementation scales or stalls.

Placement and timing. Insurance offered at the wrong moment in a user journey is invisible. Offered at the right moment, it converts at rates traditional distribution can’t match. In the UK, embedded partnerships have demonstrated the potential to reduce customer acquisition costs by up to 75%, according to the Open and Embedded Insurance Observatory’s 2024 Insight Report. The principle holds in Africa: the integration point matters more than the product design.

Regulatory clarity per market. Platforms distributing insurance need to understand whether their role constitutes regulated activity in each jurisdiction. In Nigeria, the open banking framework enables data sharing but doesn’t automatically authorise insurance distribution. In Kenya, the IRA’s sandbox framework offers a path but requires active engagement. Getting this wrong creates legal exposure that scales with every policy issued.

Infrastructure vs. build. Building embedded insurance infrastructure from scratch means managing underwriter relationships, regulatory compliance, product configuration, premium reconciliation, and servicing across every market you operate in. That’s a full insurance operations function grafted onto a platform business. The alternative is partnering with infrastructure providers that handle the insurance layer through a single API integration, letting the platform focus on serving its core customers.

The Takeaway

Embedded insurance doesn’t fail because platforms don’t want it. It fails because the product engine, underwriter network, fulfilment, and servicing layers aren’t designed for scale — and certainly not for the multi-market, multi-currency, mobile-first realities of African markets.

The platforms that move first won’t just earn commission revenue. They’ll become the distribution layer that traditional insurers depend on to reach the next hundred million policyholders. Check out real-world outcomes from platforms that have made the shift.

Ready to launch? Book a demo

Subsribe to our newsletter to receive weekly content

.svg)

{kind=link}

{kind=link}