The Embedded Insurance Playbook for Fintechs & E-commerce Platforms

If you run a fintech, neobank, online store, marketplace or travel platform, you’re probably feeling the same pressure:

- Acquisition costs keep rising

- Margins on payments, lending and logistics are thin

- Customers expect more protection, with less friction

Traditional “go to this link and buy a policy” insurance doesn’t match how digital users behave anymore. Embedded insurance does.

This playbook is for product managers, founders and digital business owners who want to:

- Unlock a new, high-margin revenue line

- Increase user trust and retention

- Reduce disputes and support tickets

…by simply adding the right protection at the right moment in their existing journeys.

What is embedded insurance, really?

Embedded insurance is when you offer insurance inside your product, at the exact moment a user is exposed to risk, not on a separate website, not days later.

Think of moments like:

- Buying a phone or laptop

- Shipping goods locally or cross-border

- Booking a flight or holiday

- Taking a loan or BNPL plan

At those points, instead of doing nothing, you add a simple prompt:

“Protect this order against loss and damage for 0.5%.”

“Add loan protection for a small monthly fee.”

The key idea: you already own the transaction and the trust, embedded insurance lets you own more of the value around that risk.

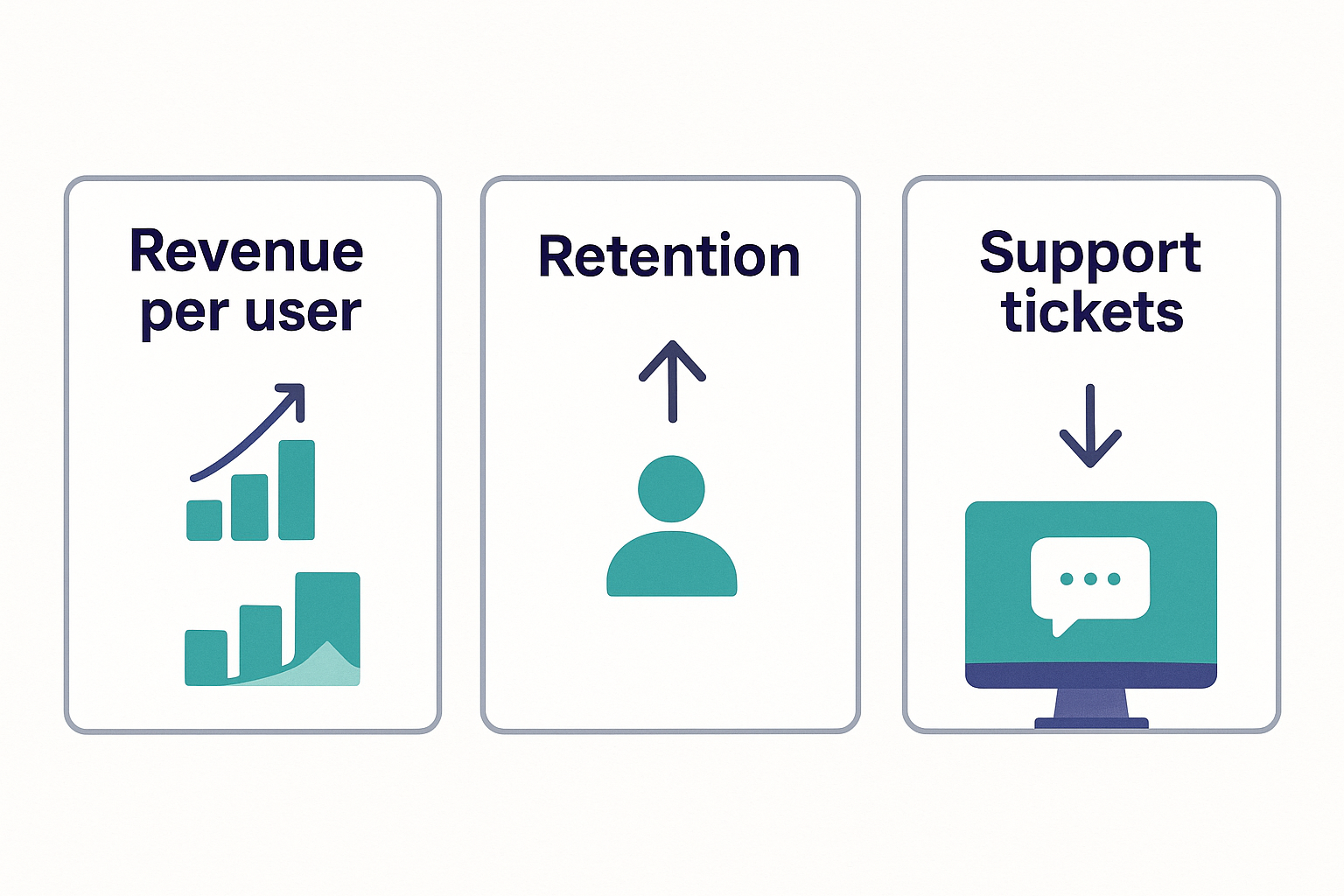

Why product teams should care

Embedded insurance isn’t just an upsell. It moves core business metrics.

1. New revenue line

- You earn commission or revenue share on each policy sold.

- Every eligible transaction becomes a chance to attach a small, high-margin product.

2. Higher LTV and stickiness

Customers who feel protected:

- Are more confident doing bigger, riskier transactions with you

- Come back more often

- Are less likely to switch to a competitor over small price differences

3. Fewer disputes and angry tickets

When something goes wrong (parcel lost, device damaged, borrower can’t repay):

- Clear cover + smooth claims = less blame on your product

- You move from “the one responsible” to “the one who made it easier to recover”

3 embedded insurance models that actually work

You don’t need every model. You need the one that fits your main journey.

1. Checkout add-on

“Protect my shipment against loss or damage for 0.5% of order value.”

Best for:

- E-commerce and marketplaces

- Logistics and fulfilment platforms

- Travel, ticketing and events

Why it works:

- The risk is obvious (loss, damage, cancellation)

- The user is already in “decision mode” with their card out

2. Bundled / default cover

Insurance is included with a plan or tier.

“Our premium account protects your card purchases and trips.”

Best for:

- Neobanks and wallets

- Merchant / SME products

- Membership and loyalty clubs

Why it works:

- Simple narrative: “This plan keeps you covered.”

- Great for differentiating higher-tier bundles.

3. Embedded in lending flows

Loan protection that pays off balances if the borrower dies or can’t work due to covered events.

Best for:

- Digital lenders and BNPL

- Micro-lending and working capital products

Why it works:

- Protects both the borrower and your portfolio

- Makes taking the loan feel safer and more responsible

How to find your first embedded insurance use case

You don’t have to launch five products in three markets. Start with one clear, high-impact opportunity.

- Map your core journeys

Onboarding, checkout, shipping, loan application, disbursement, repayments.

- Mark the “anxiety moments”

Where would a user reasonably think: “What if this goes wrong?”- High-value purchases

- Fragile or time-sensitive shipments

- New loans or BNPL plans

- Travel bookings or events

- Score each opportunity

- Transaction volume

- Average value / risk size

- How painful a bad outcome would be for the user

- Pick one journey for a pilot

For example: shipment protection at checkout, or loan protection at disbursement.

What good UX looks like (so people actually turn it on)

Most embedded insurance fails because of poor UX, not poor economics.

Keep it:

- Short – One clear benefit sentence: “Protect your order against loss and damage.”

- Honest – Simple bullets for what’s covered and what’s not.

- Fast – One tap to add or skip.

- Mobile-first – Designed for small screens and low attention spans.

Trust boosters:

- Show who underwrites the cover (even if your brand is front and centre).

- Set realistic expectations: “Most valid claims are paid within X days.”

- Let users easily find their policy and claims info in-app later.

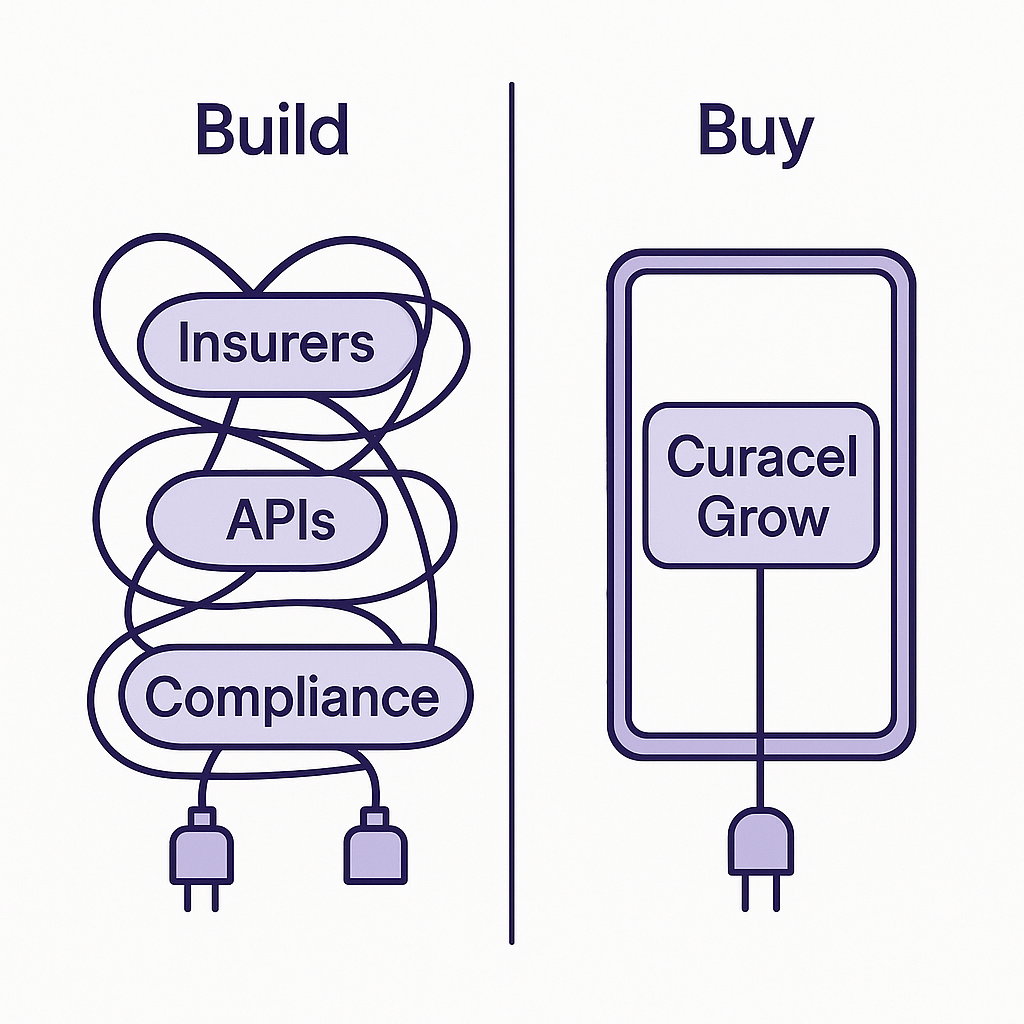

Build vs buy: why platforms use Curacel Grow

You can build an embedded insurance stack yourself, but you’ll need to:

- Integrate with insurers across countries

- Design and maintain policy + claims APIs

- Handle compliance, reporting and ongoing operations

- Support teams when claims and edge cases happen

That’s months of work for product, engineering, legal and ops.

Curacel Grow is designed to shortcut that.

With Curacel Grow, fintechs and platforms can:

- Plug into ready-made insurance products built for digital businesses

- Integrate via simple APIs / SDKs for policies and claims

- Go live in multiple markets with pre-integrated insurers

- Track attach rate, revenue and claims performance through dashboards

How to get started

If you’re a fintech or platform and embedded insurance is on your roadmap (or you’re just curious), here’s a simple way to move forward:

- Choose one journey

For example:- Shipment protection at checkout

- Device protection for card purchases

- Loan protection at disbursement

- Estimate the upside

Use a simple ROI calculator for embedded insurance based on your volumes and average transaction values to see the revenue potential. - Request a Curacel Grow demo or sandbox

Explore available products, see how the APIs fit your stack, and sketch your first pilot. - Run a pilot, then scale

Launch with a segment or market, measure attach rate and revenue, then expand across more journeys and regions

You can learn more and request a demo at curacel.co/contact-us.

Abonnez-vous à notre newsletter pour recevoir du contenu hebdomadaire

.svg)